The Consumer Finance Protection Bureau (CFPB) recently announced their proposed rule to ban medical bills from credit reports— an important step in mitigating the harm of medical debt for millions of people across the country. While not all providers furnish medical debt to credit reporting agencies, this will tremendously impact those who do.

Are Medical Bills Being Removed From Credit Reports?

Making changes to credit reporting is a long process, and medical bills are not yet officially being removed from credit reports. The CFPB kicked off this rulemaking process in September 2023, following years of effort from advocates at the state and federal level and proposed the rule in full on June 11, 2024; the agency is taking public comment in the federal register through August 12, 2024. The rulemaking process can vary but in general after receiving public comment the CFPB will process those comments, conduct an internal review, and publish the final rules. In the interim, it is important to provide feedback on where the public would like to see changes before the rules are made official.

Understanding Medical Bills on Credit Reports

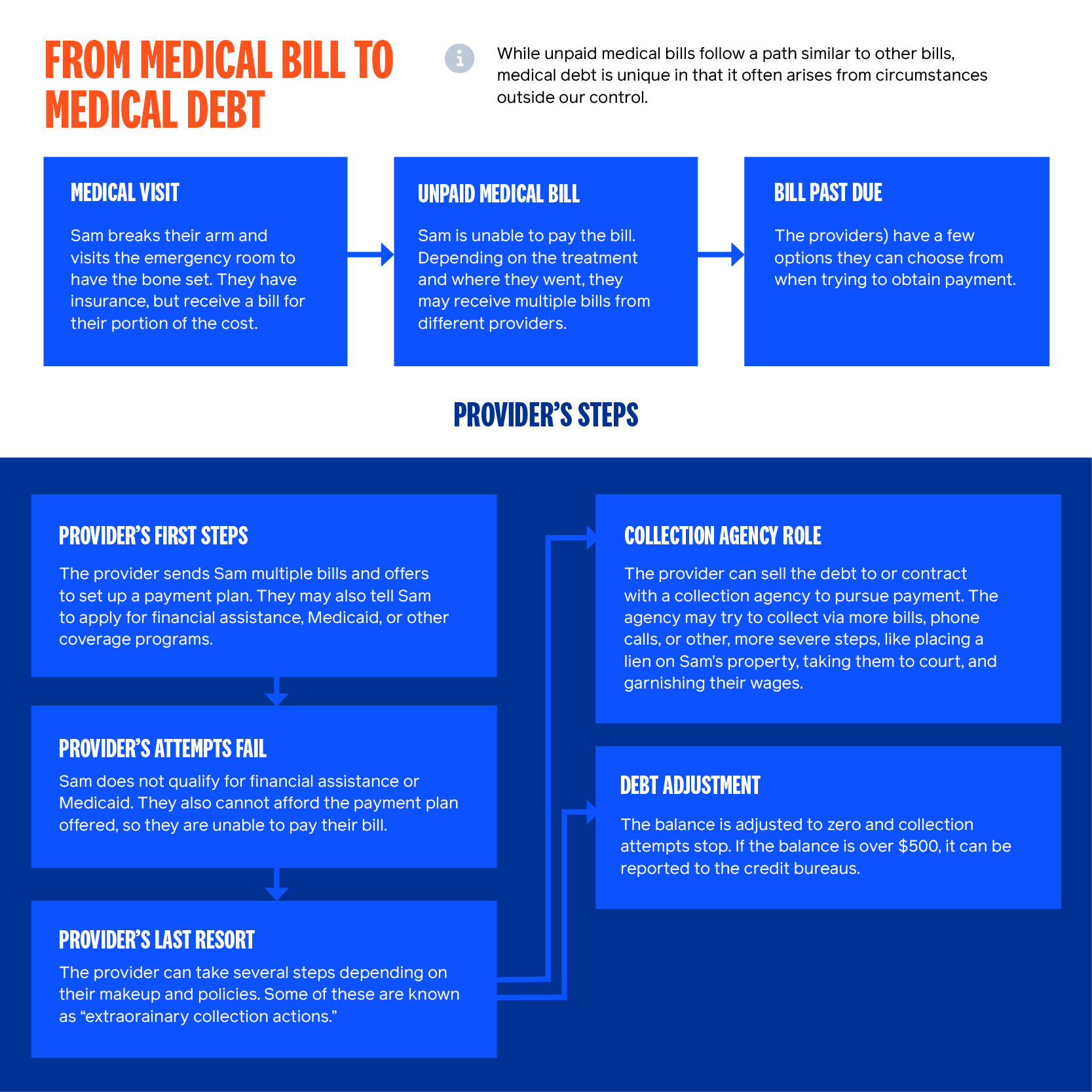

Not all providers furnish medical debt to credit reporting bureaus, and a voluntary move by the Big 3 credit reporting agencies to stop reporting medical bills under $500 in collections helped decrease—but did not eliminate—the burden of medical debt on people’s credit scores. If the medical debt is over $500, the debt collector or provider practice can report it to a credit bureau, at which point the patient has 180 days to resolve the bill before it is included on their credit history; it will appear on their credit report as an “account in collections” and can have a significant impact on their credit score. The general path from medical bill to medical debt (and potentially a mark against your credit score) is outlined in the graphic below:

Research shows that medical debt is not a good predictor of creditworthiness and using it as such disproportionately impacts Black communities, people with disabilities, and other historically marginalized groups. We here at Undue Medical Debt applaud CFPB’s proposed ban on medical bills on credit reports and are excited to see where these changes will lead. However, erasing medical debt from credit reports does not eliminate the problem of medical debt— and in order to tackle the problem, we need to know how big it is and continue monitoring it.

Tracking the Scale of Medical Debt After the End of Credit Reporting

We must fully eliminate medical debt from credit reports, and we must also create an alternative way to access more accurate data. We don’t know the true extent of the medical debt crisis because many of these debts wind up on credit card balances, second mortgages, predatory payday loans, on kitchen counters—parsed out and tucked away wherever people can find a few dollars to pay down their bills. Fortunately, there are a number of efforts at the state, federal, and even organizational levels that could be leveraged to create a national database on medical debt:

- The Survey of Income and Program Participation (SIPP, part of the Census Bureau) has been tracking medical debt since 2018, when it added a question asking respondents whether they had “medical bills [they were] unable to pay in full”;

- The CDC’s National Health Interview Survey (NHIS) now includes questions around challenges paying medical bills;

- Public health departments across the country are beginning to monitor medical debt as a social determinant of health (SDOH), with Los Angeles County creating an entire program to address the crisis;

- Hospital systems are considering including medical debt in their community health needs assessments; and

- Kaiser Family Foundation (KFF) in collaboration with Kaiser Health News tracks the patient’s experience of medical debt through surveys and storytelling. Many nonprofits—including Undue—replicate these questions in their own survey work.

These questions, however, only scratch the surface. We must use these as a foundation for creating a more robust panel of questions—and thus data—for patients, providers, and the collection and financial industry to fully appreciate the scope of the crisis. There are existing data collection efforts at the federal level such as the Medical Expenditure Panel (MEPs) or the National Health Interview Survey (NHIS) where the government could build off existing questions and provide a deeper understanding of the prevalence and disproportionate harm of medical debt. In addition to surveys, future work could include partnering with providers to receive direct information from them on the amount of debt in collections and where patients are struggling to pay. Removing medical debt from credit reports is a win for patients, but it is not a cure. We must commit to making sure medical debt is not hidden from view.

The Case to Erase Medical Debt Completely

Still, it is important to celebrate our wins, and this is a big one! According to the CFPB’s own estimate, this rule could remove as much as $49 billion of medical debts currently driving down credit scores for 15 million people in the United States. If the rule is finalized, they note people with medical debt still on their credit reports can expect to see their credit scores increase by an average of 20 points; earlier voluntary moves from the three major credit bureaus to quit reporting medical debts under $500 already saw average credit scores for people with medical debt rise from subprime (below 600) to near prime (between 601 and 660).

The CFPB’s proposed rule could go even further; in its current form, this rule only bans the use of medical debt on credit reports for financial lenders—it does not ban the use of medical debt on credit reports for things like renting an apartment or finding employment. Fully removing medical debt from people’s credit reports means millions nationwide would have an easier time getting a mortgage, buying a car, and even getting a job— all things medical debt should never have an impact on in the first place. No one should struggle to find a place to live or get a job simply because they got sick or were in an accident.

Banning credit reporting is an important step in mitigating the harms of medical debt. We know from our own research that people want to pay their medical bills; indeed, they often make difficult trade-offs to pay what they can, but high costs, unexpected medical bills, and unbalanced cost-sharing leave many with unmanageable bills. Even with an increase in credit scores, medical debt’s hydra of harms remains; aggressive providers and collection agencies can still sue patients, send letters, make phone calls, place liens on property, and garnish wages. Many people pay for their care using credit cards, meaning a substantial amount of medical debt is already hiding on credit reports. Finally, the mental health burden of medical debt is intense; fear and anxiety around medical debt is enough to lead nearly half of all adults to defer care, trapping many in a cycle where they need more intense, expensive treatment down the line—leaving them with the very medical debt they were trying to avoid.

A great deal of work remains to fully transform our healthcare system into an equitable, affordable, and accessible resource. Interventions like medical debt abolishment, removing adverse credit reporting, and other policy changes are important tools that help us ease the burden while we work to build a system where no one is forced to choose between physical and financial health simply to get the care they need.