Get help with medical bills or debt

In Connecticut, 1 in 3 people experience financial burdens due to medical bills. Anyone can face medical debt after an accident, illness, or emergency even if you have insurance. It often comes without warning and can happen to people who did everything “right.”

Find resources to help afford the cost of healthcare or help with unpaid bills.

Medical Bills and Debt

Medical debt is one of the most common forms of financial hardship in the United States. In Connecticut, 1 in 3 people have financial burdens due to medical bills — even people who have insurance.1 High costs and a confusing healthcare system can leave patients with bills they did not expect and cannot afford. Anyone can face medical debt after an accident, illness, or emergency. It often comes without warning and can happen to people who did everything “right.”

What is Medical Debt?

Medical debt is money people owe for medical or dental care that they can’t afford to pay. This can include unpaid bills from hospital care, doctor visits, or dental work. It can also include debt from payment plans, credit cards, bank loans, or money borrowed from family or friends to pay for healthcare. More than 100 million people in the U.S. have faced healthcare debt in the last five years,2 with more than $220 billion owed nationwide.3

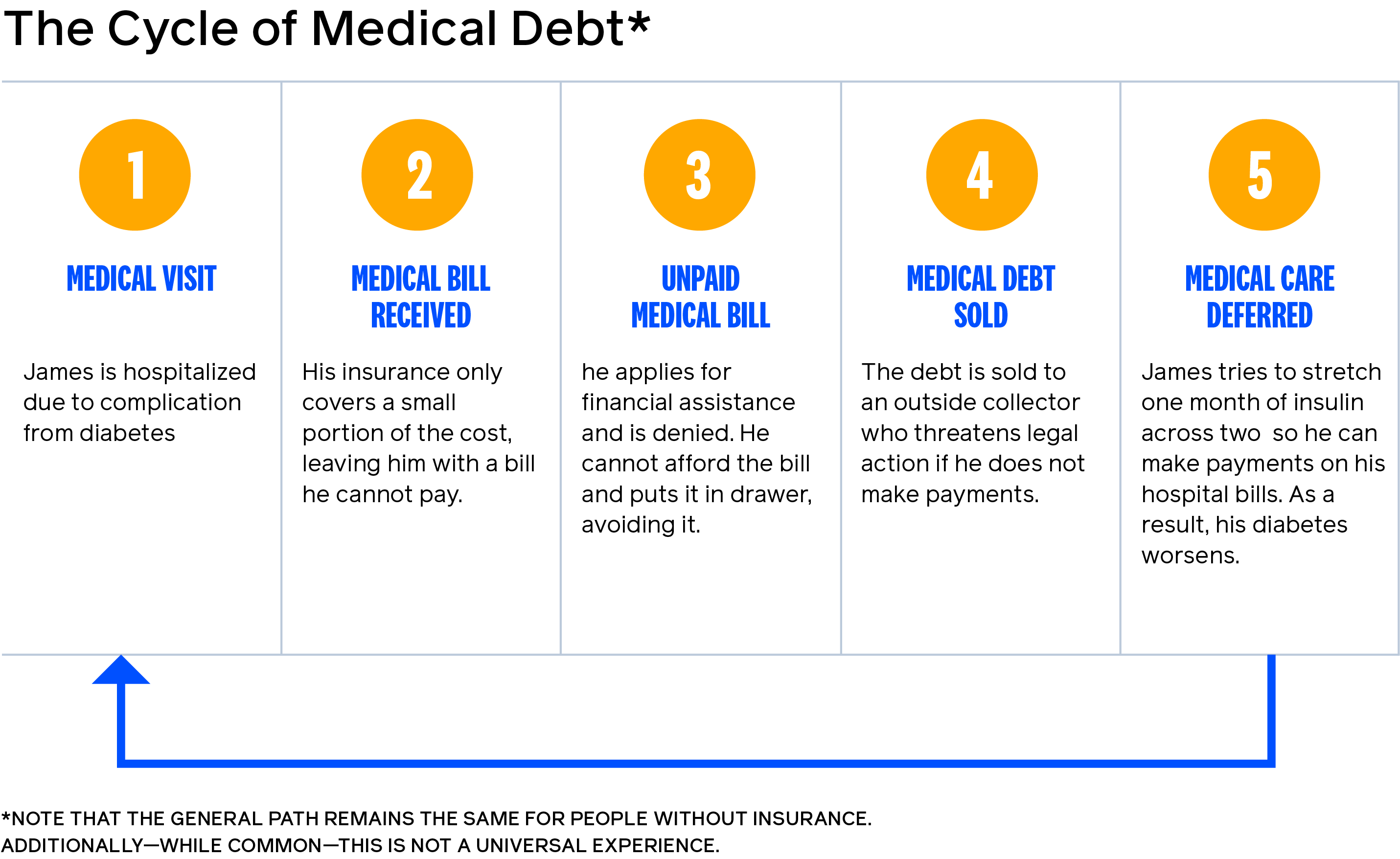

Most medical debt starts with a surprise — an accident, a sudden illness, or a hospital stay. For people with chronic conditions like cancer or diabetes, medical debt can be ongoing. Over time, unpaid bills can pile up and make it hard to pay for essential expenses like housing, food, and utilities. Medical debt affects health, finances, and peace of mind. Here’s what often happens:

The Cycle of Medical Debt

- A national poll from 2025 found more than one-third of respondents (35%) currently owe money or have debt due to medical or dental expenses — with more than half saying they worry about going into debt when using medical services.4

- Medical debt is common. Most of the bills people struggle to pay (66%) stem from a one-time or short-term event like a car accident or hospital stay.5

- Medical debt is not only a financial burden. It can also cause people to delay or skip needed healthcare. In Connecticut, 61% of residents report that they, or a family member, skipped or delayed medical care due to cost.6

Medical Debt Rules in Connecticut

Rules to protect patients from medical debt vary widely from state to state. Protections in Connecticut include:

- You Have the Right to Emergency Care No Matter What

Under the federal Emergency Medical Treatment and Labor Act (EMTALA), hospitals must screen and treat you in an emergency even if you do not have insurance or cannot pay. Hospitals cannot delay your care to ask about your insurance or payment method. - Free and Reduced-Cost Care Is Available at Connecticut Hospitals

All nonprofit hospitals must offer financial assistance programs that provide free and/or discounted care. Each hospital sets its own rules about who qualifies for these programs. Beginning 10/1/26, hospitals will have to include certain financial assistance information on each billing statement. Some hospitals also have “free bed funds” that can assist patients who are having difficulty paying their bill. - Medical Debt Cannot Hurt Your Credit Score in Connecticut

Hospitals and providers cannot report unpaid medical bills to credit bureaus. Medical debt should not appear on your credit report or lower your credit score. Collection companies working for hospitals must follow this rule too.7 - Hospitals and Providers Cannot Require a Card to be on File Before Your Visit

Hospitals cannot require a credit card, debit card, or bank account number before you receive care. Hospitals and providers can request that information, and you can choose to share, but it cannot be a condition of getting treatment.8 - Limits on What Hospitals Can Bill Certain Uninsured Patients

If you make less than 250% of the federal poverty level ($39,900 per year as a single person or $68,300 for a family of three in 2026) and if you aren’t eligible for public health insurance, hospitals and health systems cannot collect more than the “cost of providing services.”9 - Protection from Surprise Medical Bills and Upfront Cost Estimates

Under the federal No Surprises Act, you can’t be charged out-of-network costs for out-of-network care in an emergency — such as emergency room visits and air ambulance services — and if you are uninsured or self-pay, providers must give you a good-faith estimate of expected costs before scheduled care or when you ask for it. - Hospitals Cannot Make You Sell Your Home

Hospitals and hospital-affiliated providers cannot foreclose on your primary home to collect medical debt, but they may place a lien on your home to collect a past medical debt once the home is sold.10 - Limits on Interest in Lawsuits for Hospital Debt

If you are sued by a collection agency or hospital for a hospital debt, state law limits pre- and post-judgment interest charged on the debt to 5% per year, and the court gets to decide whether to charge interest at all.11

What You Can Do to Reduce or Eliminate Your Medical Debt

Right now, many people are left to navigate a complex, confusing, and costly healthcare system on their own. If you have a medical bill that you cannot pay or did not expect, help is available.

Don’t skip care to avoid debt. Keep taking medications and seeing your doctor. Avoiding care often leads to worse (and more expensive) outcomes down the road.

Quick Tips

Download our short guide on navigating medical bill.

Know your Coverage

- If you’re insured:

- Understand your deductible, copays, and whether you need prior approval before seeking care.

- Check to see if providers are in-network. Going to an in-network provider generally costs less.

- Once you have a bill, make sure your insurance was correctly applied before you pay the bill.

- Uninsured? You may qualify for Medicaid (HUSKY Health), a plan through your employer, or a subsidized plan through Access Health CT, Connecticut’s ACA Health Insurance Marketplace.

- Learn about the different insurance plan options.

Reduce or Eliminate the Bill

- Apply for financial assistance. This should be your first step if your bill is from a hospital or hospital-affiliate.Bills may be reduced or completely erased. You may qualify even if you have insurance, are working, your bill is over a year old, or you don’t qualify based on your income but have a lot of medical debt.

- Avoid paying with a credit card unless you can pay it off immediately. Paying with credit cards, including medical credit cards, turns medical debt into regular debt and removes medical debt-specific protections.

- Ask for a payment plan. If you don’t qualify for free or discounted care through a hospital’s financial assistance program and to avoid putting debts on a credit card, ask for a low or no-interest payment plan directly with the provider; only agree to payments you can realistically afford.

Know your Rights

- Learn more about your rights under the Fair Debt Collection Practices Act (FDCPA) which makes it illegal for debt collectors to use abusive, unfair, or deceptive practices when they collect debts.

- If you’re sued, do not ignore a lawsuit. Consult an attorney or a legal aid organization about whether to answer, contest the bill, or explore other options, including bankruptcy.

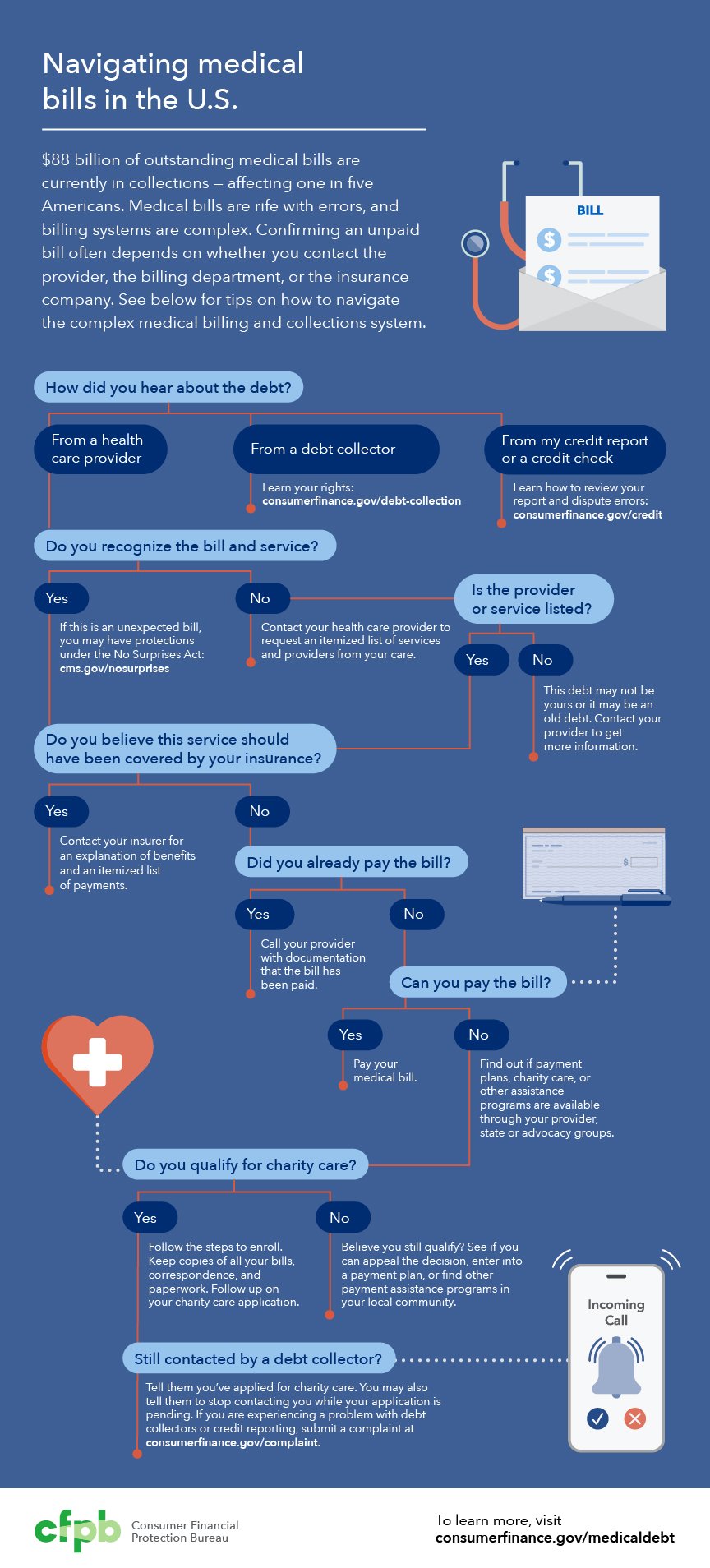

Navigating Medical Bills in the U.S.

CFPB: Consumer Financial Protection Bureau

To learn more, visit consumerfinance.gov/medicaldebt

More Help with Medical Bills

Open and Organize Your Bill(s)

- Open the bill as soon as it arrives and confirm it’s addressed to you (or your minor child). Medical bills can be overwhelming, but it’s best not to avoid bills associated with medical care.

- Check the due date to avoid late fees.

- Keep all bills, letters, and insurance papers in one place.

Tip: If you have insurance, check whether the paper you received is a bill or an Explanation of Benefits (EOB). An EOB is not a bill.

An EOB shows what your insurer was charged, what they paid, and what you potentially owe. The actual bill will come from the provider.

Eliminate or Reduce Hospital Bills with Financial Assistance

- All nonprofit hospitals in Connecticut must offer financial assistance. Many for-profit hospitals and other providers may also offer financial assistance with similar eligibility standards.

- Find the hospital’s financial assistance policy or get help applying for financial assistance. Bills can sometimes be reduced — or wiped out completely.

- You may qualify even if you have insurance, are working, your bill is over a year old, or if you have a lot of medical debt.

- Mention other bills and financial stress you’re facing. You might be eligible for a discount if you have significant medical debts or other pressing financial burdens.

Avoid Using Credit Cards to Pay Healthcare bills

- Putting healthcare bills on a credit card (including medical credit cards like CareCredit) turns medical debt into regular debt and removes certain medical debt-specific protections.

- Payment plans can be a much better option, especially since some hospitals charge low or no interest.

Verify the Bill’s Accuracy

The system is complex, and medical billing errors can occur. Before you make payments, verify that insurance was properly applied and charges are accurate.

Confirm Insurance was Billed

- Mistakes can happen. Providers can make a mistake when typing in your insurance ID number, name, or date of birth, and the bill will not process through your insurance correctly, or providers might send you a bill before your insurance has applied their adjustments or payments.

- TIP: If you have a hyphenated last name, pay extra attention to make sure both the provider and your insurance are using the complete and correct sequence and spelling of your last name.

- Check the bill for line items like “insurance adjustments” or “billed to insurance” to confirm whether your insurance coverage has been applied.

- Call your insurance or provider to understand what your insurance covers.

TIP: When calling a billing office or insurer, write down the date, time, the name of the person you spoke with, and what they told you. Keep this log with your bill documents.

Learn about common denial reasons and what you can do.

Learn about the prior authorization process and the rules in Connecticut.

Review an Itemized Bill

- If you need more detail, call the provider’s billing office to request an itemized bill.

- You have a right to your itemized bill because this document is part of your medical records. HIPAA (Health Insurance Portability and Accountability Act of 1996) gives you the right to see and get a copy of your health information.

- You cannot be refused access to your health information because you haven’t paid your bill.

- Review every line of your itemized bill carefully for errors, such as:

- Charges for care you did not receive

- Duplicate charges

- In-network providers billed as out-of-network

- Preventive care that should have been covered by insurance

- Consider contacting a patient representative: call the hospital’s main number and request to be connected to a Patient Representative, or the Patient Services department to get technical support reviewing your bill.

Negotiate Payment Plans and Settlements

Medical providers are often willing to negotiate unpaid bills.

- Contact the provider’s billing department and ask for an interest-free payment plan.

- If you are uninsured or paying out-of-pocket, many providers will offer a reduced rate — ask for the self-pay or cash rate.

- Be honest with your provider or collector. If paying will cause real hardship, say so. Mention other bills and financial stress you’re facing.

- Get a copy of the written terms of any payment plan.

- Review this manual for more tips on negotiating bills.

If a Bill Goes to Collections, Don’t Ignore It

- Collectors must follow the Fair Debt Collection Practices Act, which bans harassment, threats, and misleading tactics.

- Know your rights — request written “validation information” of the debt before agreeing to any payment, as harassment or misleading tactics are illegal.

Get Legal Help

- If you are sued, do not ignore it. Consult an attorney or legal aid organization, about whether to answer, contest the bill, or explore other options, including bankruptcy.

- If you think a provider didn’t follow the rules for discounts, free care, or debt collection, or you are being unfairly pursued by a debt collector, legal help might be needed.

- Legal aid organizations provide free legal services related to medical debt for people with low incomes.

Connecticut Legal Services: https://ctlegal.org/

Go-to resource for low-income Connecticut residents who need free civil legal help and expert legal representation and advocacy.

Statewide Legal Services of Connecticut: https://slsct.org/

Free legal helpline for income-eligible Connecticut residents who need guidance on their rights and options —such as how to dispute a bill, negotiate a payment plan, or challenge an insurance denial.

Additional Support and Resources

The healthcare system is complex, with many professionals specializing in different areas of the same system. Use the links below to find professionals and resources who can help.

Connecticut State Office of the Healthcare Advocate (OHA) — Helpful links and resources

Affordable Care and Prescription Options

- Community Health Centers and Federally Qualified Health Centers (FQHCs) – Use this tool to search by location and find a nearby federally-funded community health center that provides primary medical and dental care to people of all ages, whether or not they have health insurance, with services offered on a sliding fee scale based on ability to pay.

- ArrayRX – A free Connecticut discount card, available through the Access Health CT website, that helps uninsured or underinsured residents save significantly on prescription drug costs at participating pharmacies statewide. Note: ArrayRX may be used as an alternate discount source for some medications, but it does not replace insurance or prevent Medicare late enrollment penalties.

- Cost Plus Drug Company – A free tool to browse low-cost generic medications and have prescriptions filled and shipped directly to your door at cost — with no hidden fees.

- NeedyMeds.org – Search this database for help paying for medications. Enter the name of the medication you are seeking financial help for, and browse by prescription assistance programs, drug discounts, and low-cost clinics. Each program has its own qualifying criteria, but coupons are largely available for all.

- GoodRX – A free tool that lets you compare prescription drug prices at nearby pharmacies and access coupons that can dramatically lower your out-of-pocket medication costs, even if you have insurance.

- Connecticut State Dental Association Community Dental Clinics – A directory of community dental clinics across Connecticut where residents can find low-cost or sliding-scale dental care close to home.

- Finding Dental Care | National Institute of Dental and Craniofacial Research – A tool that helps patients who are uninsured, underinsured, or on a tight budget find affordable or free dental care options in their area, including community health centers, dental schools, and government programs.

- Health Care – United Way of Connecticut – 211 and eLibrary – Use this phone number (2-1-1) to get connected to local help with food, utilities, rent, transportation, healthcare, and crisis support.

Additional Patient Advocacy and Financial Support Organizations

- Dollar For – A free service to help find out if you qualify for hospital financial assistance (aka hospital charity care) and to assist you with applying if you are likely eligible.

- Patient Advocate Foundation – A national nonprofit that helps patients navigate insurance denials, access financial assistance, and resolve workplace or coverage issues that arise from a serious diagnosis.

- Cancer Financial Assistance Coalition – A searchable database connecting cancer patients with financial assistance programs that can help cover treatment costs, medications, transportation, and other expenses related to their diagnosis.

- HealthWell Foundation – This nonprofit helps people who qualify pay for insurance costs such as copays, deductibles, or premiums for certain diseases.

- Debt collection | Consumer Financial Protection Bureau – Use this resource to learn your rights when dealing with debt collectors, including how to recognize illegal practices, dispute a debt, and file a complaint.

This project was supported, in whole or in part, by federal award number 21.027 awarded to State of Connecticut by the U.S. Department of the Treasury

- Connecticut Survey Respondents Receive Unexpected Medical Bills and Incur Medical Debt; Express Bipartisan Support for Government Action – Healthcare Value Hub ↩︎

- 100 Million People in America Are Saddled With Health Care Debt – KFF Health News ↩︎

- The burden of medical debt in the United States – Peterson-KFF Health System Tracker ↩︎

- Voters Show Strong Bipartisan Support for Policies that Protect People from Medical Debt – Undue Medical Debt ↩︎

- The Burden of Medical Debt: Results from the Kaiser Family Foundation/New York Times Medical Bills Survey | KFF ↩︎

- Connecticut Survey Respondents Struggle to Afford High Health Care Costs; Worry about Affording Health Care in the Future; Express Bipartisan Support for Policy Solutions – Healthcare Value Hub ↩︎

- CT Gen Stat § 19a-673b. (2024) ↩︎

- CT Public Act 25-97, Section 4 (2025) ↩︎

- CT Gen Stat § 19a-673 (2019) ↩︎

- CT Gen Stat § 19a-673b. (2024) ↩︎

- CT Gen Stat § 37-3a. (2024) ↩︎