In a time of intense political rancor, medical debt stands out as a rare unifying issue. We know more than 100 million people contend with debt from medical or dental bills, often making tremendous trade-offs just to make ends meet; the reasons for this are many, ranging from the failures of insurance coverage to confusing and opaque billing practices and a broken healthcare financing system. Recent policy developments moved things in the wrong direction, but there is reason for hope. Undue Medical Debt partnered with PerryUndem to test voter reactions to specific policies addressing medical debt, and the results are striking—voters of all political affiliations want their elected officials to act to address medical debt and there is near unity on how they want it to be addressed.

Every policy we tested had support, but a few rose to the top with 90% or more of respondents in favor; to that end, Undue Medical Debt is releasing a series of briefs taking a deeper dive into those policies.

Policy Focus: Limit Interest Rates on Medical Debt

The problem.

Medical debt is rarely planned or voluntary, unlike other sources of debt that might accrue interest. Charging interest on an already unaffordable medical bill risks pushing people deeper into debt—if I am struggling to afford a $200 bill from my provider, charging interest on that debt makes it less likely for me to be able to pay it back. By some estimates, more than 66% of people who filed for bankruptcy did so due to medical debt; high interest rates are a contributing factor, often driving people deeper into a cycle of debt (taking out payday loans, using credit cards with even higher interest rates, etc.) that is nearly impossible to escape. If the amount of debt owed grows beyond $500, it is more likely to be reported to credit bureaus, which in turn lowers credit scores and makes it much harder to access non-predatory loans to try and pay down that debt.

While many providers do not charge interest on medical debt, some do— or they contract with third party debt collectors who do. Most states lack specific laws regarding how much interest hospitals and debt collectors can charge on medical debt, but all states have some type of usury law (which sets the absolute maximum interest rate a lender can charge). These can vary wildly, from 5% to more than 20%, but they can also be overridden by contract law. According to National Consumer Law Center (NCLC), general post-judgment interest laws can be as high as 12%, meaning the amount I owe a provider is essentially doubled after five years. Our healthcare financing system already puts a tremendous amount of administrative burden on the patient and expecting them to also understand the peculiarities of contract law while trying to navigate the morass of insurance, billing, and personal health challenges sets the entire system up for failure.

State approaches.

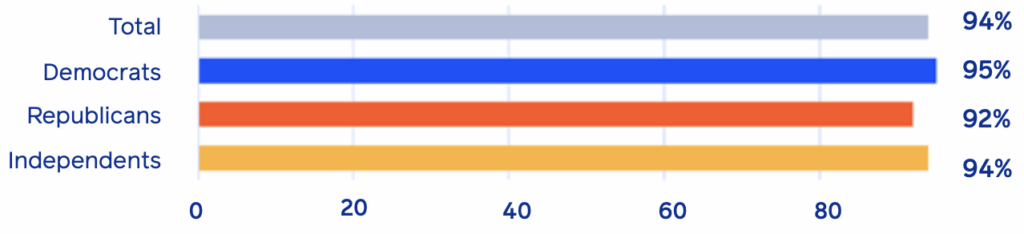

As discussed above, charging interest on an already unaffordable bill only pushes people deeper into debt. An astounding 94% of voters support banning or capping interest rates on medical debt, recognizing that increasing the amount owed does not make it easier or more likely for someone to pay. We know people generally want to pay back their medical bills, and putting guardrails around when, whether, and how much interest can be charged carves out space for people to do this without their debt snowballing and being driven to bankruptcy.

Strong, bipartisan support for limiting interest rates on medical debt.

Legislative efforts at the state level are growing, with most laws being passed in the last few years. A total of 13 states currently regulate medical debt interest rates, with the laws typically taking one of three forms: a total ban on charging interest, caps on interest, and limitations on who can be charged interest and when. A brief overview of each type of legislation is provided below.

Bans on charging interest.

This is the newest approach, with two states passing laws since 2023. Delaware’s Medical Debt Protection Act bans charging interest or late fees on medical debt, regardless of any agreements to the contrary, while Maine’s update to their Fair Debt Collection Practices Act bans debt collectors from charging interest on medical debt and categorizes it as an unfair and deceptive practice. Both bills were effective in the first half of 2024, meaning the full extent of their impact is not yet clear.

Capping interest.

Passing a total ban on charging interest may not be politically feasible in some states, in which case passing reasonable caps is a good alternative. Arizona overwhelmingly passed a 3% cap on interest rates for medical debt via ballot initiative in 2022, while North Dakota limits interest to 1% or $25/month. Notably, emerging research indicates interest rate caps should be combined with time-limited repayment windows to make sure these payments are affordable—otherwise some patients essentially become trapped in interminable payments with a debt that never diminishes.

Limiting who can be charged interest and when.

The third most common approach typically pairs interest rate caps with limits on who can be charged interest—Colorado passed legislation in 2023 reducing their interest rate cap from 8% to 3% and banning charging interest on patients eligible for financial assistance, while New Jersey’s Louisa Carmen Act contains provisions that prohibit medical creditors and debt collectors from charging more than 3% interest per year. Virginia is one of the most recent states to address medical debt interest rates, passing legislation that prohibits creditors from charging interest or late fees until 90 days after the final invoice and capping that interest at 3% per year.