2025 Pulse Survey

Healthcare Access, Affordability & Medical Debt from the Perspective of Debt Relief Recipients

Introduction

Healthcare costs continue to poll as a top affordability priority across the U.S.; six in ten worry they cannot cover costs associated with a serious illness and nearly half worry they cannot afford routine healthcare costs.1 These concerns persist across income and party affiliation.2 About 100 million adults currently have unpaid medical bills and, collectively, carry nearly $200 billion in medical debt.3 Projections by Third Way estimate that planned federal cuts to healthcare spending could expose an additional 5 million people to medical debt and increase Americans’ collective medical debt by $44 billion.4,5 Medical debt is more than a pocketbook issue: fear of unpaid medical bills results in worse healthcare outcomes for children and adults alike.6

To bridge the immediate relief of medical debt erasure with our long-term policy goals,7 Undue launched a rapid pulse survey of 2025 debt relief recipients.8 While these descriptive findings reflect the self-reported, lived experiences of 153 respondents rather than a representative national sample, they provide vital, real-time insights to support policymakers, philanthropy and advocates working to end medical debt. Additional qualitative findings will be available later this summer.

Background

Undue’s 2025 pulse survey – a short, rapid survey of Undue debt relief recipients – highlights three core insights from people who received medical debt relief:

- Medical debt risk is universal: Both insured and uninsured individuals incur medical debt and avoid care to avoid debt. Among respondents, nearly one in three struggled with bills they expected insurance to cover. Undue’s broader portfolio data reinforces this vulnerability: more than half of individuals receiving debt relief in 2025 were insured when their medical debt was incurred.

- Hospital financial assistance is hard to access: Hospital financial assistance policies are frequently unknown or difficult to navigate, and many people who can’t afford their medical bills still do not qualify for help. At the time of the survey, 61% of respondents were unaware that non-profit hospitals were required to offer financial assistance, and among the 25% who did apply before their medical debt was erased, 79% were denied.

- Medical debt drives widespread financial and emotional strain: Household stress comes in many forms and can negatively impact both a family’s balance sheet and their mental health; 76% reported harassment from creditors and debt collectors, while 62% experienced increased anxiety or depression after incurring the medical debt that was later erased.

2025 Pulse Survey Findings

1. Universal risk: insured patients struggle.

The survey reinforces existing research showing that patient cost-sharing portions lead to unaffordable out-of-pocket costs, worse health outcomes and financial distress.9,10

Out-of-pocket costs drive debt even for the insured.

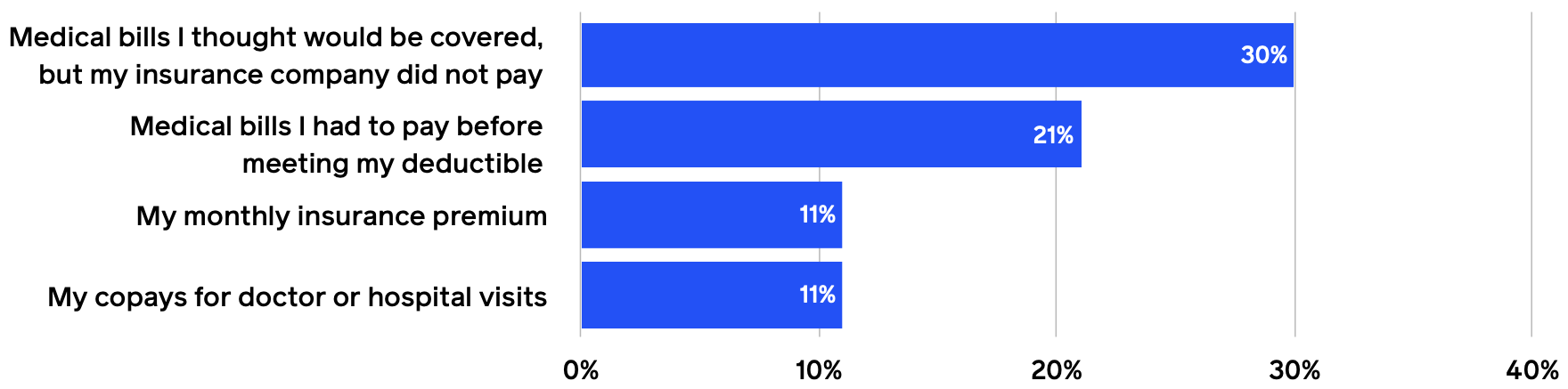

Among debt relief recipients surveyed in early 2026, 82% were insured at the time of the survey. Yet, nearly one in three said the biggest healthcare cost challenge in the past 12 months were medical bills they thought would be covered by insurance, while an additional 21% cited medical bills they had to pay before meeting their deductible—showing that insurance is not protecting people’s financial security.11

Beyond survey respondents, more than half of Undue’s total 2025 debt relief went to people who had insurance when they incurred their debt. This further confirms the limits of insurance coverage to help people avoid medical debt. Furthermore, 75% have bills that are past due or that they were unable to pay, as well as bills in collections (70%).

Insurance comes with its own costs.

The chart below reinforces that out-of-pocket costs tied to insurance are among the biggest healthcare cost burdens respondents faced.

When thinking about your healthcare expenses from the past 12 months,

which of these was the biggest challenge for you and your family?

A clear majority of respondents (63%) place the primary blame for their medical debt on insurance companies. This echoes the 63% finding in Undue’s national poll of 2024 voters representing Republicans, Democrats and Independents, demonstrating that survey respondents and the broader electorate share the conclusion that insurance is not providing adequate coverage.

2. Hospital financial assistance is hard to access, even for eligible patients, leading to potentially avoidable debt.

Evidence from multiple studies aligns with what respondents reported to Undue: financial assistance programs are not accessed due to low awareness and the misperception that it’s not for them.12, 13

Hospital financial assistance remains unknown to many patients.

At the time of the survey, six in ten respondents (61%) did not know most hospitals are required to offer financial assistance. Among those who did not apply before their medical debt was erased, the most common reason – cited by 76% of respondents – was simply not knowing assistance was available, followed by thinking they would not qualify (29%). What debt relief recipients shared with Undue reinforces research showing most people never learn about financial assistance.

Patients who could be eligible for financial assistance end up taking on debt to pay their bill.

Prior to receiving relief, many respondents attempted to manage their medical bills through other means: 22% used provider payment plans, 22% borrowed from family or friends and 20% used credit cards. Nearly a quarter (24%) did not attempt payment at all, and a smaller percent turned to payday loans (8%). In addition, roughly one in three reported waiting until absolutely necessary to seek care to avoid the risk of debt.

I was in a constant battle with the credit bureau and the collection agency every year because they sold the debt every year to a new agency so my credit took a hit each January as if it was a new bill.

— David

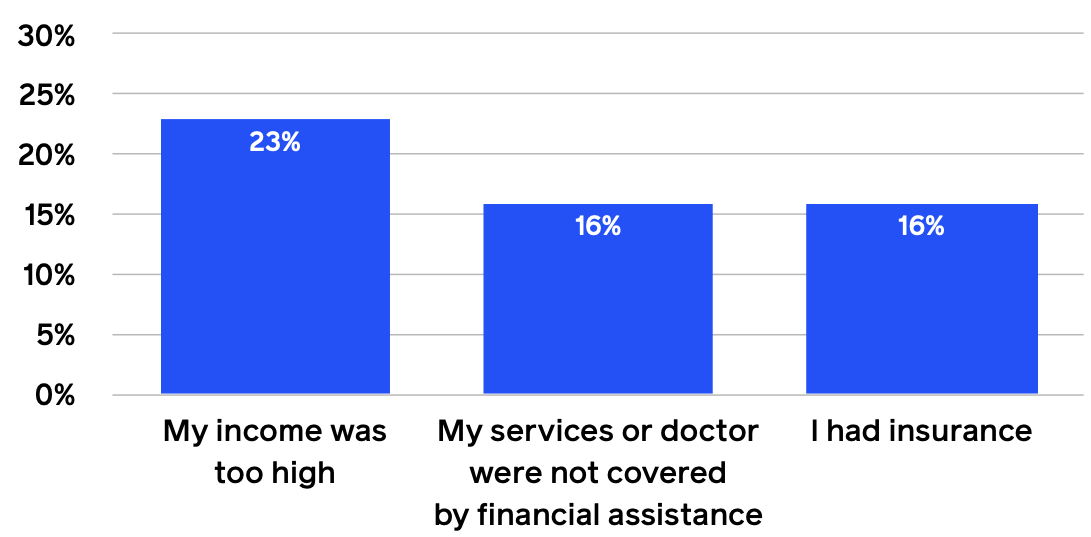

Some respondents reported being ineligible for a hospital’s financial assistance even though they could not afford their medical bill.

Typically, hospital financial assistance covers free care for people making up to 200% of the federal poverty level—or $62,400 for a family of four.14 This threshold leaves many families exposed to debt. The chart below describes reasons people reported being ineligible for financial assistance.

Why were you denied financial assistance?

“I was told since I had insurance my discount was applied when insurance settled.”

— MICHELLE

3. Medical debt drives widespread financial and emotional strain.

Third-party research consistently shows that medical debt is a leading source of financial instability and stress, contributing to credit damage, material hardship and delayed care—findings reinforced by what patients tell Undue.15

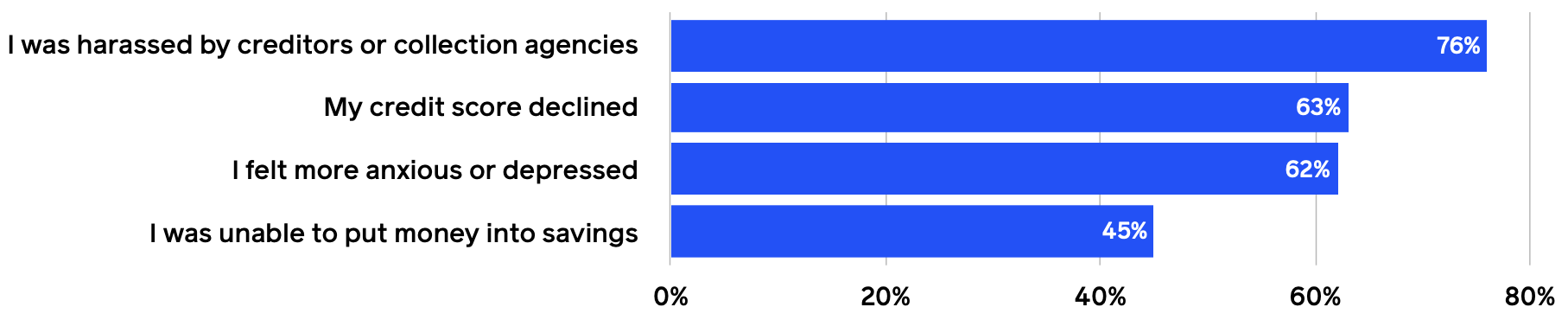

People face significant negative financial and personal impacts.

As the chart below illustrates, most respondents experienced significant financial challenges prior to debt relief.

What effects did this medical debt have on you, if any, before it was erased?

For some, the consequences affected basic needs and long-term stability –

26% reported cutting back on food or buying cheaper groceries and 10% said

medical debt prevented them from continuing their education. In the past 12 months, a significant share of respondents reported delaying payment of a medical bill (55%), delaying or skipping doctor visits (50%), and experiencing pain due to delayed care (48%).

Respondent Perspectives on the Impact of Debt Relief

The following responses illustrate the perspectives of debt relief recipients on the benefits of debt relief; they are not intended as causal or generalizable findings.

Many respondents described debt relief as providing immediate financial breathing room and greater flexibility in meeting basic needs. When asked about the impact on their budgets, nearly six in ten (59%) reported that following relief, their household was able to prioritize spending on other important needs. 87% said essential expenses such as food, rent, utilities and transportation, more than half (53%) said medical expenses such as filling a prescription or going to therapy and about one-third (32%) reported being able to save for emergencies or retirement.

Respondents also described meaningful emotional and informational impacts. A majority reported feeling less alone after receiving their debt relief letter (76%), along with increased confidence engaging with hospitals and providers (65%) and a better understanding of how to navigate the healthcare system (63%).

These experiences extended to how some respondents approach care. Over half reported being more likely to take prescribed medications (57%) and get routine medical care (66%)—services that many had previously delayed due to cost concerns.

Taken together, these perspectives illustrate how medical debt shapes day-to-day financial and healthcare decisions, and how relief is experienced by recipients as a source of financial stability and support amidst an ongoing affordability crisis.

More from Undue

- Saad, L. (2026, April 28). Affordability still dominates Americans’ financial worries. Gallup. https://news.gallup.com/poll/708905/affordability-dominates-americans-financial-worries.aspx ↩︎

- Harty, A., & Cousens, M. (2026, March 9). Special Report: Views on health care in the battleground and beyond. Navigator. https://navigatorresearch.org/views-on-health-care-in-the-battleground-and-beyond/ ↩︎

- Fulford, S.L., & Wilson, E. (2025). Medical debt and collections in the United States. Health Affairs Scholar 3(8). https://doi.org/10.1093/haschl/qxaf159 ↩︎

- Kendall, D., Elliot, B., & Kusuma, T. (2025, June 23). GOP Health Care Cuts: A recipe for medical debt disaster. Third Way. https://www.thirdway.org/memo/gop-health-care-cuts-a-recipe-for-medical-debt-disaster ↩︎

- Park, E. (2025, August 14). New CBO Health Coverage Estimates of Budget Reconciliation Law. Georgetown University McCourt School of Public Policy. https://ccf.georgetown.edu/2025/08/14/new-cbo-health-coverage-estimates-of-budget-reconciliation-law/ ↩︎

- Sparks, G., Lopes, L., Montero, A., Presiado, M., & Hamel, L. (2026, April 30). Americans’ Challenges with Health Care Costs. KFF. https://www.kff.org/health-costs/americans-challenges-with-health-care-costs/ ↩︎

- Undue Medical Debt. (2026). 2026 Policy Priorities. https://unduemedicaldebt.org/wp-content/uploads/2026/04/POLICY_PRIORITIES_2026-1.pdf ↩︎

- Between January and April 2026, Undue Medical Debt surveyed 2025 medical debt relief recipients who opted into being contacted by Undue. Of 672 individuals, 199 responded (29.6%) and 153 completed the survey (76.9% completion rate among respondents, 22.8% of the total sample). Respondents skewed female (70%), with 27% identifying as male and 3% as non-binary. Age ranged from 18-75+, with the largest share falling between 35-54 years old (56%). Racially and ethnically, 62% identified as white, 27% as Black or African American, and 12% as Hispanic or Latinx. In 2025, Undue abolished over $9.9 billion in medical debt for approximately 6.5 million individuals. ↩︎

- Braga, B., McKernan, S.-M., Atherton, S., & Martinchek, K. (2025, November 20). Debt in America: An Interactive Map. Urban Institute. https://apps.urban.org/features/debt-interactive-map/?type=overall&variable=totcoll ↩︎

- Blavin, F., Braga, B., Johnson, N., & Wekulom, A. (2024, July 10). The Changing Medical Debt Landscape in the United States. Urban Institute. https://apps.urban.org/features/medical-debt-over-time/ ↩︎

- PwC Health Research Institute. (2025). Behind the Numbers 2026: Medical Cost Trends. PricewaterhouseCoopers. https://www.pwc.com/us/en/industries/health-industries/library/behind-the-numbers.html ↩︎

- Kona, M. (2024). Making Financial Assistance Programs Equitable and Accessible. JAMA Internal Medicine, 184(10), 1148-1149. https://doi.org/10.1001/jamainternmed.2024.3561 ↩︎

- Messac, L., Janke, A.T., Rogers, L.H., Fonfield, I., Walker, J., Rushbanks, E., Becker, N.V., & Bai, G. (2024). US Nonprofit Hospitals Have Widely Varying Criteria to Decide Who Qualifies for Free and Discounted Charity Care. Health Affairs, 43(11), 1569-1577. https://doi.org/10.1377/hlthaff.2023.01615 ↩︎

- American Hospital Association. (2020, October 15) Patient Billing Guidelines. https://www.aha.org/system/files/media/file/2020/10/Patient-Billing-Guidelines.pdf ↩︎

- Aborode, A.T., Oginni, O., Abacheng, M., Edima, O., Lamunu, E., Folorunson, T.N., Oko, CI.I., Iretiayo, A.R., Lawal, L., Amarachi, R., Badri, R., Bamigbade, G.B., Olanrewaju, O.F., Agwuna, F.O., & Adesola, R.O. (2025). Healthcare Debts in the United States: A silent fight. Annals of Medicine and Surgery, 87(2), 663-672. https://doi.org/10.1097/MS9.0000000000002865 ↩︎

About Undue

Undue is a national nonprofit and has cancelled over $40 billion in medical debt for over 27 million people as of March 2026. The organization purchases portfolios of medical debt from providers like hospitals and debt buyers for a fraction of their face value with support from private donors and local and state governments.

Undue’s work is both immediate and systemic:

it stops the financial

harm of existing debt

while also advancing policy changes that prevent medical debt from occurring in the first place.